This project involves using a combination of statistics along with financial thoery to demonstrate a popular trading strategy used in equity markets: Pairs Trading.

Our goal involves the following:

- Part 1: Creating a model that test for stationarity.

- Part 2: Creating a model that test for cointegration.

- Part 3: Assigning a portfolio of assests and testing for a cointegrated pair among the dataset.

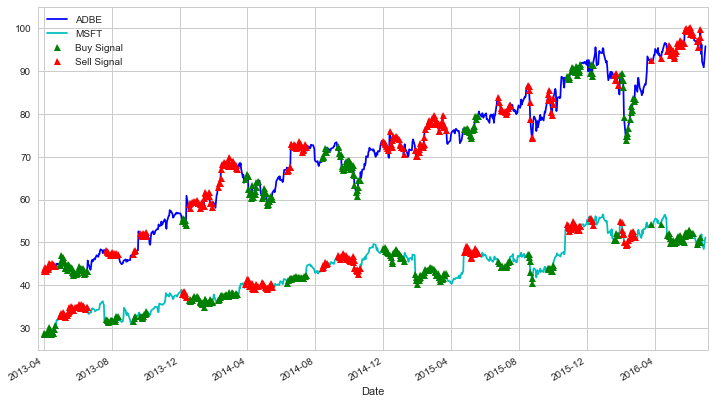

- Part 4: Establishing features and labels that will allow us to create trading signals for the strategy.

I used the data from Yahoo Finance, which provides historical financial data for free. This data was extracted via the yFinance Python module.

- Jupyter NoteBook

- Numpy

- Pandas

- Matplotlib

- Seaborn

- Statsmodels

- Pandas DataReader

- DateTime

- yFinance (formally known as

Fix Yahoo Finance)